That new car smell is calling your name, isn't it? But before you drive off into the sunset, a big question looms: should you lease or finance? It's a decision that can impact your wallet and your driving experience for years to come. Let's navigate this road together.

Choosing how to acquire a vehicle can feel like navigating a maze. Are you worried about long-term commitment? Maybe you're concerned about depreciation? Or perhaps you're just trying to figure out the most cost-effective way to get behind the wheel of your dream car. All those monthly payments, interest rates, and the fine print in those agreements can feel overwhelming and leave you feeling uncertain about making the right choice.

This guide is designed to help you understand the key differences between leasing and financing a vehicle, so you can make an informed decision that aligns with your financial situation, driving habits, and personal preferences. We'll break down the pros and cons of each option, explore the hidden costs, and provide practical tips to help you drive away with confidence.

Ultimately, the best choice – leasing or financing – depends on your individual circumstances. Leasing offers lower monthly payments and the option to drive a new car more often, but comes with mileage restrictions and no ownership. Financing, on the other hand, builds equity and allows for unlimited mileage, but requires a larger down payment and higher monthly payments. Understanding these trade-offs is crucial. We'll also delve into aspects like maintenance, insurance, and long-term costs associated with both options. Whether you're eyeing a sleek sports car or a family-friendly SUV, this guide will equip you with the knowledge to make the right vehicle acquisition decision.

Understanding Leasing: The Short-Term Commitment

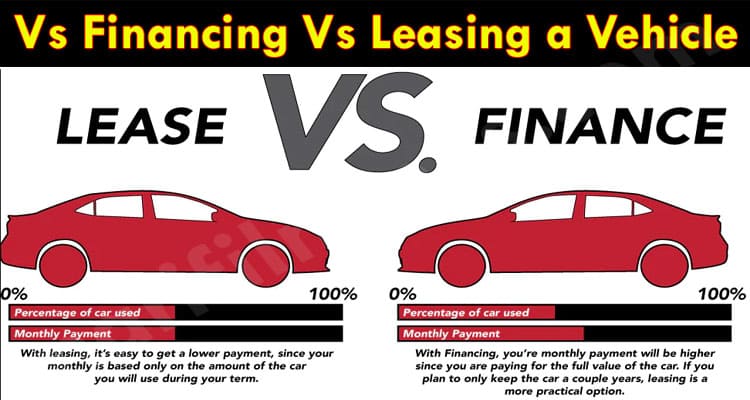

Leasing a vehicle is essentially like a long-term rental. You pay for the depreciation of the car during the lease term, plus interest and fees. My own experience with leasing was a mixed bag. I leased a sporty little hatchback when I was fresh out of college. The low monthly payments were incredibly appealing, allowing me to drive a car I otherwise couldn't afford. However, I quickly learned about the mileage restrictions the hard way! A few unplanned road trips later, and I was facing overage charges. It was a valuable lesson in understanding the fine print. Leasing is ideal for those who like to drive a new car every few years and don't want the hassle of selling or trading in a vehicle. You're essentially paying for the portion of the car's value you use during the lease period. When the lease is up, you simply return the car. This can be attractive if you enjoy having the latest technology and features without the long-term commitment. It also offers predictability, as you know exactly what your monthly payment will be for the duration of the lease. However, keep in mind that you won't own the car at the end of the lease, and you'll be subject to mileage limitations and potential wear-and-tear charges. Carefully consider your driving habits and whether you're comfortable with these restrictions before opting for a lease.

Understanding Financing: Building Ownership

Financing a vehicle means taking out a loan to purchase the car. You make monthly payments over a set period, and once the loan is paid off, you own the vehicle outright. This is a more traditional approach to car ownership. When you finance, you're building equity in the vehicle, meaning you're gradually increasing your ownership stake with each payment. This can be a significant advantage if you plan to keep the car for a long time, as you'll eventually own it free and clear. Financing also offers the freedom to drive as much as you want, without worrying about mileage restrictions. You can customize the car to your liking and sell it whenever you choose. However, financing typically involves a larger down payment and higher monthly payments compared to leasing. You're also responsible for the vehicle's maintenance and repairs throughout its lifespan. The total cost of financing, including interest, can also be higher than leasing in the long run. Before financing, carefully consider your budget, credit score, and long-term transportation needs. Make sure you can comfortably afford the monthly payments and the associated costs of ownership.

The History and Myths of Leasing and Financing

The concept of leasing vehicles actually dates back to the early 20th century, when companies began offering "rental" agreements for commercial vehicles. It wasn't until the 1960s that leasing became more widely available to consumers. Financing, on the other hand, has been around for much longer, evolving alongside the growth of the automotive industry. One common myth is that leasing is always more expensive than financing. While it's true that you don't own the car at the end of a lease, the lower monthly payments can make it an attractive option for those on a tight budget. Another myth is that financing is always the better long-term investment. While you do build equity with financing, the car's value depreciates over time, which can offset the benefits of ownership. It's important to consider all factors, including your individual circumstances and the specific vehicle you're interested in, before making a decision. Understanding the history and debunking these myths can help you approach the leasing vs. financing decision with a more informed perspective. Don't let preconceived notions cloud your judgment; instead, focus on what makes the most sense for your financial situation and driving needs.

The Hidden Secrets of Leasing and Financing

Beyond the advertised monthly payments and interest rates, there are often hidden costs and fees associated with both leasing and financing. With leasing, be aware of potential charges for excess mileage, wear and tear, and early termination. These fees can add up quickly and significantly increase the overall cost of the lease. It's crucial to carefully inspect the vehicle before returning it to avoid unexpected charges. With financing, consider the potential for higher interest rates if you have a lower credit score. Also, factor in the costs of maintenance, repairs, and insurance, which can be substantial over the life of the loan. Another hidden secret is the negotiation power you have when leasing or financing. Don't be afraid to negotiate the price of the vehicle, the interest rate, and the terms of the lease or loan. Researching the vehicle's market value and comparing offers from different dealerships can help you get the best possible deal. By being aware of these hidden costs and negotiating effectively, you can avoid unpleasant surprises and make a more financially sound decision.

Recommendations for Choosing the Right Option

The best recommendation is to carefully assess your individual needs and circumstances before making a decision. Ask yourself these questions: How long do I plan to keep the car? How many miles do I drive each year? What is my budget? What are my long-term financial goals? If you value driving a new car every few years and don't drive excessively, leasing might be a good option. If you prefer to own your vehicle, drive a lot of miles, and want the freedom to customize it, financing might be a better fit. It's also wise to compare offers from multiple dealerships and lenders. Get pre-approved for a loan to understand your interest rate options. Read the fine print of both lease and financing agreements carefully before signing anything. Don't be afraid to ask questions and seek clarification on any points you don't understand. Consider consulting with a financial advisor to get personalized advice based on your specific financial situation. Ultimately, the right choice is the one that aligns with your needs, budget, and long-term goals.

Evaluating Your Driving Habits

Your driving habits play a significant role in determining whether leasing or financing is the right choice for you. If you typically drive less than 10,000-12,000 miles per year, leasing might be a more attractive option, as you're less likely to exceed the mileage restrictions. However, if you drive significantly more than that, financing might be a better choice to avoid costly overage charges. Consider your daily commute, weekend trips, and any other regular driving activities. Also, think about whether your driving habits are likely to change in the future. For example, if you're planning a cross-country road trip, financing would likely be a more suitable option. Evaluate your driving patterns over the past few years to get a realistic estimate of your annual mileage. This will help you make an informed decision about which option best aligns with your driving needs. Remember that exceeding the mileage limits on a lease can result in substantial penalties, so it's important to choose an option that accommodates your driving habits.

Tips for Negotiating a Lease or Loan

Negotiating a lease or loan can seem intimidating, but it's an essential part of the car-buying process. One of the most important tips is to do your research beforehand. Know the market value of the vehicle you're interested in and compare offers from different dealerships. Get pre-approved for a loan to understand your interest rate options. When negotiating, focus on the total cost of the lease or loan, not just the monthly payment. Pay attention to the interest rate, fees, and any other charges. Don't be afraid to walk away from a deal if you're not comfortable with the terms. Dealerships are often willing to negotiate to close a sale, so don't settle for the first offer you receive. Be polite but firm, and be prepared to counteroffer. Consider negotiating the price of the vehicle itself, even when leasing. A lower vehicle price will result in lower monthly payments. Also, be aware of any incentives or rebates that you may be eligible for. By following these tips, you can increase your chances of getting a fair deal on a lease or loan.

Understanding Credit Scores and Interest Rates

Your credit score plays a significant role in determining the interest rate you'll receive on a car loan. A higher credit score typically translates to a lower interest rate, which can save you thousands of dollars over the life of the loan. Before applying for a car loan, check your credit score and review your credit report for any errors. If you have a low credit score, consider taking steps to improve it before applying for a loan. This could involve paying down debt, making timely payments, and avoiding new credit applications. Even a small improvement in your credit score can make a big difference in the interest rate you qualify for. Shop around for the best interest rate by comparing offers from different lenders. Credit unions often offer more competitive rates than traditional banks. Don't assume that the interest rate offered by the dealership is the best available. By understanding the relationship between credit scores and interest rates, you can make informed decisions and save money on your car loan.

Fun Facts About Leasing and Financing

Did you know that the average lease term is around 36 months? Or that some luxury car brands offer lease options with mileage allowances as high as 15,000 miles per year? Leasing is particularly popular in certain regions of the country, such as California and Florida, where consumers tend to prioritize driving newer vehicles. Financing, on the other hand, is more common in areas where people prefer to own their cars for a longer period. Another interesting fact is that the value of a car typically depreciates the most during the first few years of ownership. This is why leasing can be an attractive option, as you're only paying for the portion of the car's value that depreciates during the lease term. Understanding these fun facts can provide a broader perspective on the leasing and financing landscape. It's also interesting to note that the popularity of leasing and financing can fluctuate depending on economic conditions and consumer preferences. Keep these facts in mind as you weigh your options and make a decision that aligns with your individual circumstances.

How to Determine the True Cost of Ownership

Determining the true cost of ownership goes beyond just the monthly payments. With financing, you need to factor in the down payment, interest rate, loan term, insurance costs, maintenance expenses, and potential repair bills. With leasing, you need to consider the monthly payments, security deposit, mileage restrictions, potential wear-and-tear charges, and any fees associated with early termination. To get a comprehensive picture, create a spreadsheet and list all the potential costs associated with each option. Research the average maintenance and repair costs for the specific vehicle you're interested in. Get quotes from multiple insurance companies to compare rates. Consider the potential resale value of the vehicle if you're financing. Use online calculators to estimate the total cost of the loan, including interest. By carefully analyzing all the potential costs, you can make a more informed decision about which option is truly more affordable in the long run. Don't underestimate the importance of factoring in unexpected expenses, such as repairs or accidents. These can significantly impact the true cost of ownership.

What If Your Needs Change After Leasing or Financing?

Life is unpredictable, and your needs may change after you've already leased or financed a vehicle. If you've leased a car and your mileage needs increase, you may be able to purchase additional miles or negotiate a new lease agreement. However, this can often be expensive. If you've financed a car and can no longer afford the payments, you may be able to refinance the loan, sell the vehicle, or explore options like voluntary repossession. Refinancing can help you lower your monthly payments, but it may also extend the loan term. Selling the vehicle can help you pay off the loan, but you may not be able to recoup the full amount you owe. If your needs change significantly, it's important to explore all available options and carefully weigh the potential consequences. Consider seeking advice from a financial advisor or car loan expert to help you navigate the situation. Remember that communication is key. Contact your lender or dealership as soon as you anticipate a problem to explore potential solutions.

Top 5 Factors to Consider: Leasing vs. Financing

Here's a quick list to keep in mind as you make your decision:

- Budget: What can you realistically afford for monthly payments and upfront costs?

- Mileage: How many miles do you typically drive each year?

- Ownership: Do you want to own the vehicle at the end of the term?

- Flexibility: Do you prefer to drive a new car every few years?

- Long-term Goals: How does this decision align with your overall financial plan?

By carefully considering these factors, you can narrow down your options and choose the vehicle acquisition method that best suits your individual needs.

Question and Answer Section:

Q: What happens if I exceed the mileage limit on my lease?

A: You'll be charged a per-mile fee for every mile over the limit. This fee can range from $0.10 to $0.30 per mile or more, depending on the lease agreement.

Q: Can I customize a leased vehicle?

A: Generally, you can't make significant modifications to a leased vehicle, as you'll need to return it in its original condition. Minor cosmetic changes may be acceptable, but check your lease agreement for specific restrictions.

Q: Is it better to lease or finance if I want to build credit?

A: Financing a vehicle can help you build credit, as you're making regular payments on a loan. Leasing, on the other hand, may not have as significant an impact on your credit score.

Q: What is a lease buyout?

A: A lease buyout is when you purchase the vehicle at the end of the lease term. This can be a good option if you like the car and want to own it.

Conclusion of Vehicle Acquisition: Leasing vs. Financing - Which Option is Better for You?

The choice between leasing and financing boils down to personal preference and financial priorities. Carefully weigh the pros and cons of each option, consider your driving habits, and assess your long-term goals. Armed with the information in this guide, you're well-equipped to make an informed decision and drive away with confidence, knowing you've chosen the best path for your vehicle acquisition journey.